Nephrocare Health Services is India’s largest organised dialysis service provider.

It operates:

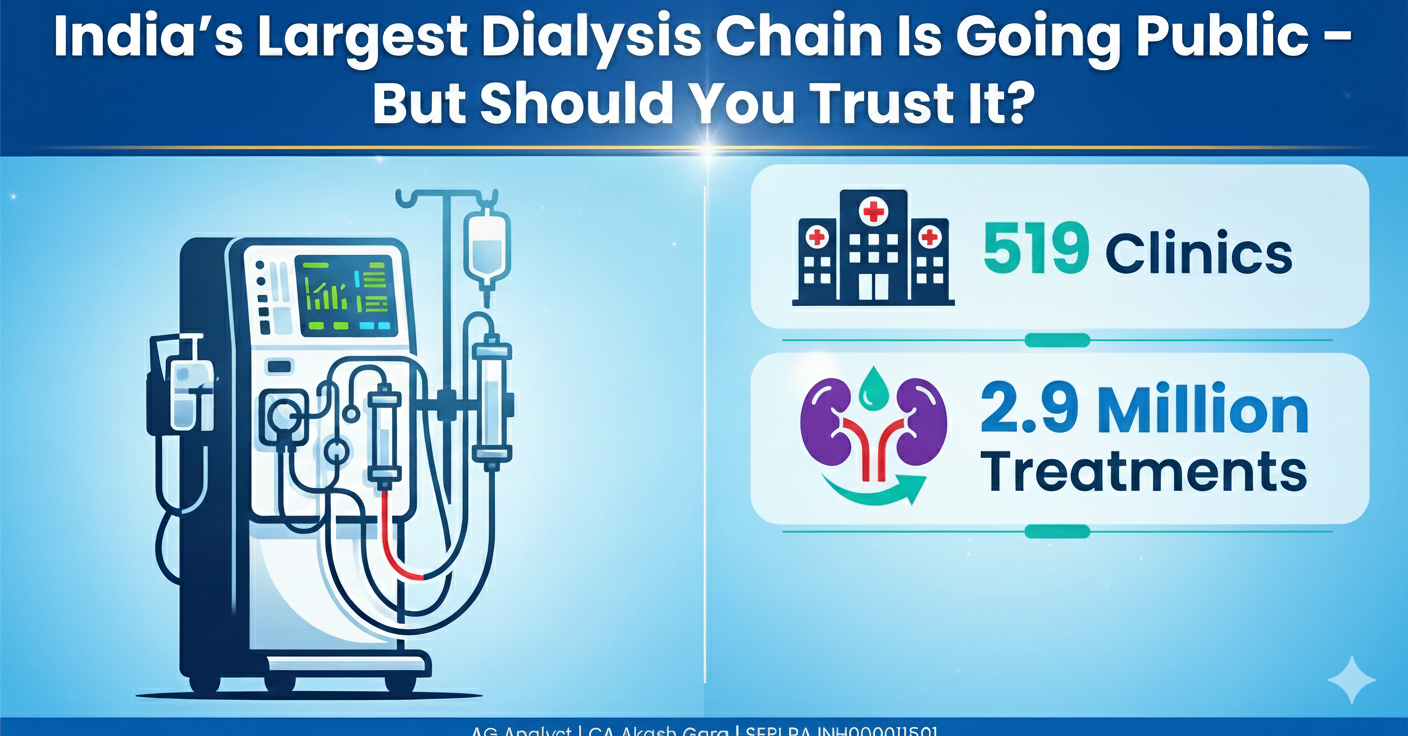

519 dialysis clinics across India & select international locations

Provides in-clinic dialysis, home dialysis, mobile dialysis, diagnostics, and pharmacy support

Completed over 2.88 million dialysis treatments in FY25

Serves almost 10% of India’s dialysis population

Dialysis is a recurring medical need, which gives the company stable, repeatable business.

Price Band: ₹438 – ₹460 per share

IPO Size: ₹871.05 crore

Fresh Issue: ~₹353 crore

OFS: ~₹517 crore

Lot Size: 32 shares

Purpose of IPO:

Open new dialysis clinics

Repayment of borrowings

General corporate purposes

Nephrocare has the widest presence among organised dialysis providers, giving scale advantage and strong brand recall.

✅ 2. Recurring Revenue Business Model

Dialysis patients require treatment multiple times a week → creates stable, predictable revenue.

✅ 3. Asset-Light Expansion (Revenue-Share Model)

Many clinics operate on partnership or revenue-share basis → reduces heavy capex burden and speeds expansion.

✅ 4. Strong Growth in Treatments & Clinics

Rapid increase in clinics and number of treatments in the last 3 years.

✅ 5. Improving Profitability

The company has recently turned profitable and improved margins due to scale benefits.

✅ 6. IPO Money Strengthens Balance Sheet

Debt repayment + expansion capital = healthier financial position + room for future growth.

✅ 7. Under-penetrated Healthcare Market

India's dialysis market is large but still underserved → long-term demand is strong.

❌ 1. Majority of Market is Unorganised

80% of India’s dialysis volumes come from small standalone clinics → pricing pressure on Nephrocare.

❌ 2. Recent Profitability Track Record

The company became profitable only recently → long-term consistent profitability is yet to be proven.

❌ 3. High Medical Staff Dependency

Dialysis requires trained technicians & nephrologists → attrition or shortage can impact service quality.

❌ 4. Working Capital Challenges

Collections from government schemes or insurance-based patients can cause delays.

❌ 5. Expansion Execution Risk

Rapid clinic expansion increases the risk of:

Low utilisation

Quality control issues

Increased overheads

Margin pressure

❌ 6. Valuation Not Very Cheap

Considering limited profit history, the IPO valuation may feel slightly stretched unless future growth is very strong.

| Company | Category | Comparison |

|---|---|---|

| Apollo Hospitals | Large premium chain | Much bigger, diversified; not dialysis-focused |

| Max Healthcare | NCR premium | Higher pricing power than Nephrocare |

| Medanta | Super-speciality | Complex cases; Nephrocare is recurring dialysis-focused |

| KIMS | Regional hospital chain | Broader care, not recurring service model |

| Nephrocare | Dialysis specialist | High scale but narrow-focused business |

Nephrocare stands out for scale in dialysis but lacks the diversification of full hospital chains.

Strengths:

✔ Massive scale in organised dialysis

✔ Recurring business model

✔ Asset-light setup

✔ Rising profitability

✔ Strong demand outlook

Concerns:

⚠ Short profit history

⚠ High competition from unorganised clinics

⚠ Execution and staffing risks

⚠ Medium valuation comfort

Long-term investors who understand healthcare and believe in India's rising chronic-care demand.

Name: CA Akash Garg

SEBI Registration No.: INH000011501

Brand: AG Analyst

I am a SEBI-registered Research Analyst.

I do not have any financial interest in Nephrocare Health Services Ltd.

I do not hold any shares of the company as of this report date.

I have not received any compensation from the company in any form.

This report is based on publicly available information and independent analysis.

This is not investment advice. Please consult your financial advisor before investing.

Stock markets are subject to risks.

Past performance does not guarantee future results.

Registered Address:

Hno. 414, Ward No. 15 , Moti

Colony , Near 999 Mobile Shop, Faridabad, Palwal, Haryana -121102

Tel: +91 9729953675 | Email: caakashgarg97@gmail.com

Grievance Officer: CA Akash Garg

Email: caakashgarg97@gmail.com

Tel: +91 9729953675

SEBI Office Details: SEBI Bhavan BKC, Plot No.C4-A, 'G' Block Bandra-Kurla Complex, Bandra

(East), Mumbai - 400051, Maharashtra

SEBI Local Office Details: NBCC Complex, Office Tower-1,

8th Floor, Plate B, East Kidwai Nagar,

New Delhi - 110023

Tel. Board: +91-011-69012998 |

E-mail : sebinro@sebi.gov.in

Tel: +91-22-26449000 / 40459000 | Fax : +91-22-26449019-22 / 40459019-22 | E-mail :

sebi@sebi.gov.in | Toll Free Investor Helpline: 1800 22 7575 | SEBI SCORES | SMARTODR |

Nism Certificate

Google Play: https://play.google.com/store/apps/developer?id=SEBI+SCORES (Or)

Search for “SEBI SCORES” in Google Play Link to SEBI Scores App

AppleStore: https://apps.apple.com/in/app/sebiscores/ id1493257302 (Or) Search

for “SEBI SCORES” in Apple App Store on website

Disclaimer: “Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors. Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. The securities quoted on the page above are for illustration only and are not recommendatory.”

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

© Copyright 2025 aganalyst.in, All Rights Reserved.